Houston has been selected as one of the hubs backed by a new program from the United States Department of Energy that's developing communities for clean energy innovation.

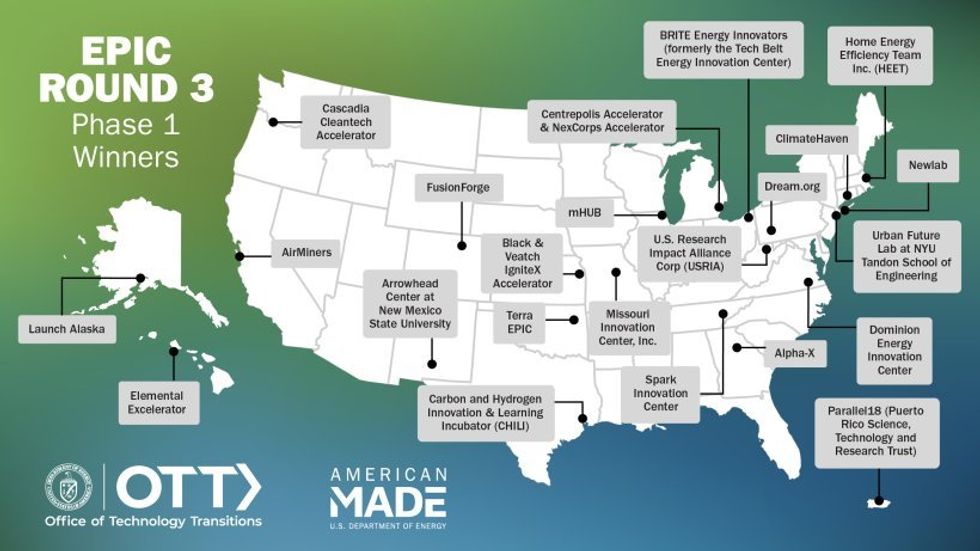

The DOE's Office of Technology Transitions announced the the first phase of winners of the Energy Program for Innovation Clusters, or EPIC, Round 3. The local initiative is one of 23 incubators and accelerators that was awarded $150,000 to support programming for energy startups and entrepreneurs.

The Houston-based participant is called "Texas Innovates: Carbon and Hydrogen Innovation and Learning Incubator," or CHILI, and it's a program meant to feed startups into the DOE recognized HyVelocity program and other regional decarbonization efforts.

EPIC was launched to drive innovation at a local level and to inspire commercial success of energy startups. It's the third year of the competition that wraps up with a winning participant negotiating a three-year cooperative agreement with OTT worth up to $1 million.

“Incubators and Accelerators are uniquely positioned to provide startups things they can't get anywhere else -- mentorship, technology validation, and other critical business development support," DOE Chief Commercialization Officer and Director of OTT Vanessa Z. Chan says in a news release. “The EPIC program allows us to provide consistent funding to organizations who are developing robust programming, resources, and support for innovative energy startups and entrepreneurs.”

CHILI, the only participant in Texas, now moves on to the second phase of the competition, where they will design a project continuation plan and programming for the next seven months to be submitted in September.

Phase 2 also includes two national pitch competitions with a total of $165,000 in cash prizes up for grabs for startups. The first EPIC pitch event for 2024 will be in June at the 2024 Small Business Forum & Expo in Minneapolis, Minnesota.

Last fall, the DOE selected the Gulf Coast's project, HyVelocity Hydrogen Hub, as one of the seven regions to receive a part of the $7 billion in Bipartisan Infrastructure Law. The hub was announced to receive up to $1.2 billion — the most any hub will get.

The DOE's OTT selections are nationwide. Photo via energy.gov

The DOE's OTT selections are nationwide. Photo via energy.gov